Ainda bem que nasci no século XX. Com as minhas preferências pelo futebol, as BMX, o jogo Risco e, depois, pela política e a aventura, se tivesse nascido algures entre 2015 e 2030 tinham-me cortado as mamas antes dos 16 anos e enchido o bandulho de hormonas sintéticas.

Sou mulher. Não me sinto mulher, tenha a condição de o ser, é o meu DNA. Não tenho um sentimento, tenho XX, um código que, por mais que eu mudasse a minha aparência, jamais se alteraria. A estes cromossomas não corresponde nenhum cérebro feminino. Da mesma forma, para o XY não existe um cérebro masculino. Como defensora dos direitos das mulheres, sempre me bati pela noção de que não há um género que corresponda a um determinado sexo. As meninas podem gostar de brincar à batalha naval e aos carrinhos, mas isso não faz delas meninos. Os meninos podem curtir bonecas ou cozinhas e isso também não faz deles meninas. Uma menina tem vagina, mas a isso não corresponde um “cérebro feminino”. Um rapaz tem pénis, mas a isso não corresponde um “cérebro masculino”. Sempre encarei esta constatação como necessária para o progresso e para a emancipação feminina e é, então, com perplexidade e temor que vejo agora difundida a ideia de que há miúdos que nascem com um “cérebro feminino” que está num corpo masculino - e que, então, é a aparência do corpo (só a aparência, já que a tal essência genética é imutável) que tem de ser alterada. Ou seja, na base da agenda trans (que pretende até que existam crianças trans, como se um menor tivesse já uma sexualidade formada e fixada) encontra-se um conceito mentiroso e perigoso, sobretudo para as mulheres e para as crianças. Como sempre, não é?

Repare-se. Seja no desporto seja até em concursos de beleza, as mulheres começam já a ser arredadas por homens que fizeram a chamada transição. Será esmagador para a natação feminina ou para o ciclismo feminino ter pessoas com biologia masculina a competir ombro a ombro com mulheres, originando uma inexorável desigualdade que arrisca eliminá-las de quase todas as modalidades. E de que mais esferas da atividade humana? O que se seguirá? Ou seja, esta ideologia não acrescenta direitos ao sexo feminino. Aniquila-os. Basta pensar na situação das mulheres detidas (obrigadas à convivência com homens biológicos), nos direitos sexuais e reprodutivos ou na violência doméstica para o entender.

Quanto às crianças, a questão ainda é mais grave. Espanha já aprovou uma “lei trans” que permitirá mudar de género a partir dos 12 anos sem parecer médico; em Portugal multiplicam-se os “prides para os pequeninos” e outras lavagens cerebrais, a par dos projetos de lei que implementam as medidas administrativas que as escolas devem adotar para promover a confusão nas crianças no que à sua identidade sexual diz respeito. Pobres miúdos que, perante este mundo cada vez mais desigual, acreditam que são estas “transições” que vão resolver as suas angústias e a sua vida sem futuro.

Aliás, esse é um dos motivos para a omnipresença da narrativa do género. Aproveitando-se da centralidade da sexualidade humana (sexualidade, não sexo), simplifica-se e tenta-se convencer meio mundo de que a chave para a sua felicidade aí reside (e não nas suas condições de vida, salários, educação), enquanto se baralham as pessoas quanto à sua identidade sexual, adiando ou até impedindo essa mesma felicidade. Mais perverso era difícil.

Tudo é sexo, excepto o sexo que é poder, lembram-se?

Autoteste

Sabe quantos milhões de portugueses vivem com menos de 660 euros por mês?

Resposta: 3 milhões - um quarto da população

Teste rápido

O unanimismo no ataque ao Ministério Público:

1) é tipo “Crime no Expresso do Oriente”, todos são culpados;

2) visa mudar o regime, atacando a separação de poderes;

3) desvia as atenções do problema principal, i.e. o regabofe do financiamento partidário;

4) é uma confissão/admissão de culpa;

5) todas as anteriores estão corretas.

Antigénio

O ataque de Rui Moreira ao Stop é um ataque à cultura, a um espaço singular e insubstituível em Portugal, uma incubadora de criatividade e experimentação. A verdadeira “Casa da Música”.

Progénio

Mesmo perante o absoluto desinteresse das grandes distribuidoras da indústria de entretenimento, “Sound of Freedom”, um filme sobre tráfico de crianças e pedofilia, continua a gerar audiências e a suscitar a curiosidade do público.

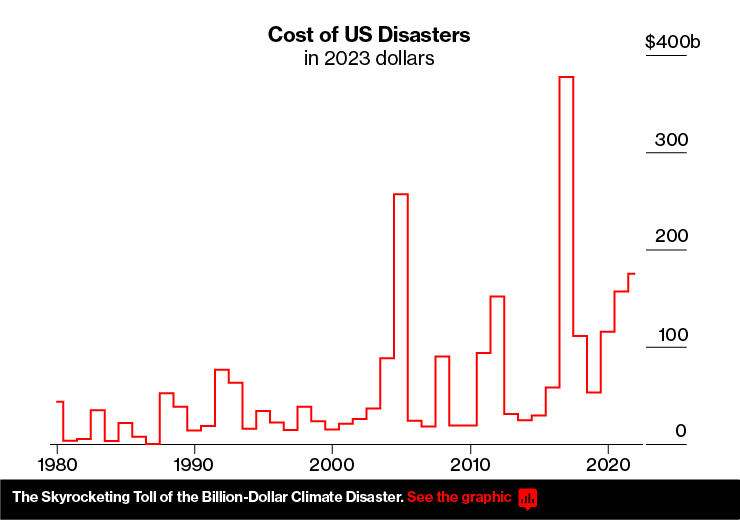

In recent months, insurance companies have announced that they’re fleeing California and Florida—states that are seeing climate change’s effects in particularly (although by no means uniquely) brutal ways.

Mortgages last 30 years, while insurance premiums are adjusted annually. When the climate was stable, Year 1 was a pretty good predictor of Year 30. But rapid warming means the perils are constantly growing, so the premium for the first year could be wildly off 10 years later, leaving homeowners at risk of far higher premiums later on. “The entire system is predicated on climate stability,” says Spencer Glendon, founder of Probable Futures, a nonprofit dedicated to climate literacy. “I think we can expect that nexus to break down soon.”

● Demographic Danger

Many people moving to risky areas are retirees thinking about little more than warm weather and lower taxes “who accelerated their retirement plans,” says Benjamin Keys, a professor of real estate at the University of Pennsylvania’s Wharton School. “They haven’t experienced a weather disaster.” It doesn’t help that most people—and developers—have short memories about destruction. Or that building codes and zoning can’t keep up.

When Farmers Insurance Group on July 12 said it would stop writing new homeowners policies in Florida, it became the 15th insurer in the state to take that step since early last year. Florida officials fault widespread insurance fraud for the exodus, but Farmers said it needed to “manage risk exposure” in a place where climate change threatens more natural disasters.

Florida’s slow-motion insurance meltdown is happening as new people pour into the places with the greatest risk of flooding, a pattern playing out across the US. Almost 400,000 more people moved into than out of the nation’s most flood-prone counties in 2021 and 2022, double the increase in the preceding two years, according to real estate firm Redfin Corp. Counties vulnerable to wildfires and heat have also seen more people arrive than leave.

Insurance cost is the main way the market signals risk to homeowners. Yet in California, Florida and Louisiana the markets are flashing warnings that homeowners are largely ignoring. “There are definitely disruptions in the feedback loop,” says Nancy Watkins, an actuary at Milliman Inc., an insurance consulting firm. Why aren’t property owners taking the hint?

● A Fundamental Mismatch

Mortgages last 30 years, while insurance premiums are adjusted annually. When the climate was stable, Year 1 was a pretty good predictor of Year 30. But rapid warming means the perils are constantly growing, so the premium for the first year could be wildly off 10 years later, leaving homeowners at risk of far higher premiums later on. “The entire system is predicated on climate stability,” says Spencer Glendon, founder of Probable Futures, a nonprofit dedicated to climate literacy. “I think we can expect that nexus to break down soon.”

● Demographic Danger

Many people moving to risky areas are retirees thinking about little more than warm weather and lower taxes “who accelerated their retirement plans,” says Benjamin Keys, a professor of real estate at the University of Pennsylvania’s Wharton School. “They haven’t experienced a weather disaster.” It doesn’t help that most people—and developers—have short memories about destruction. Or that building codes and zoning can’t keep up.

● Information Breakdown

Even when buyers seek reliable information on long-term risk, it’s hard to find, with some government maps of severe flood zones dating to the 1970s. Homeowners in those areas must purchase flood insurance to get a federally insured mortgage, but people outside the zones—or those who own their home outright—have no such requirement. First Street Foundation says some 6 million homes that should be considered at severe risk of flooding lie outside those zones. And Milliman estimates there’s $520 billion of unpriced flood loss in the housing market—a number that will only increase.

Then there’s the question of how much insurance should cost. Carly Fabian of consumer-rights group Public Citizen says buyers deserve access to average home insurance prices by ZIP code over time, which would help them assess where insurers believe risks are spiking and whether they’re paying inflated rates. But insurance companies have blocked such efforts, saying the information is proprietary. “They’ve proven unreliable narrators on climate,” Fabian says.

● The Government Backstop

In the 1960s private insurers largely pulled the plug on residential flood coverage, deeming it too risky. The federal government stepped in with the National Flood Insurance Program (NFIP), which racks up about $1.4 billion a year in losses because it can’t charge market rates. Similar state programs in California, Florida and Louisiana only insure homes that can’t get private coverage, but with insurers backing out, they’re adding customers rapidly. Florida’s Citizens Property Insurance Corp. is already the largest single insurer in the state.

The Federal Emergency Management Agency is promising reforms that will bring NFIP premiums more in line with climate risks, but Keys is skeptical. “It’s like a dad threatening to turn the car around when the kids aren’t behaving properly,” he says. “The government isn’t not going to step in and bail out people when there’s a disaster.”

● Not Yet a Deal-breaker

Premiums are rising, but so is everything else—and insurance isn’t yet expensive enough to deter buyers, with utilities and property taxes representing a bigger share of the price of a house. Even at twice the cost, insurance would “still only account for a small proportion of asset prices,” says Danny Ismail, a researcher at analytics company Green Street. But investors in mortgage-backed securities may soon start demanding coverage for the full length of the loan. “The common denominator is that risk does not really belong to the insurance companies; it belongs to the community,” Watkins says. “The insurance market is not sufficient to tackle this problem.”

When Farmers Insurance Group on July 12 said it would stop writing new homeowners policies in Florida, it became the 15th insurer in the state to take that step since early last year. Florida officials fault widespread insurance fraud for the exodus, but Farmers said it needed to “manage risk exposure” in a place where climate change threatens more natural disasters.

Florida’s slow-motion insurance meltdown is happening as new people pour into the places with the greatest risk of flooding, a pattern playing out across the US. Almost 400,000 more people moved into than out of the nation’s most flood-prone counties in 2021 and 2022, double the increase in the preceding two years, according to real estate firm Redfin Corp. Counties vulnerable to wildfires and heat have also seen more people arrive than leave.

Insurance cost is the main way the market signals risk to homeowners. Yet in California, Florida and Louisiana the markets are flashing warnings that homeowners are largely ignoring. “There are definitely disruptions in the feedback loop,” says Nancy Watkins, an actuary at Milliman Inc., an insurance consulting firm. Why aren’t property owners taking the hint?

● A Fundamental Mismatch

Mortgages last 30 years, while insurance premiums are adjusted annually. When the climate was stable, Year 1 was a pretty good predictor of Year 30. But rapid warming means the perils are constantly growing, so the premium for the first year could be wildly off 10 years later, leaving homeowners at risk of far higher premiums later on. “The entire system is predicated on climate stability,” says Spencer Glendon, founder of Probable Futures, a nonprofit dedicated to climate literacy. “I think we can expect that nexus to break down soon.”

● Demographic Danger

Many people moving to risky areas are retirees thinking about little more than warm weather and lower taxes “who accelerated their retirement plans,” says Benjamin Keys, a professor of real estate at the University of Pennsylvania’s Wharton School. “They haven’t experienced a weather disaster.” It doesn’t help that most people—and developers—have short memories about destruction. Or that building codes and zoning can’t keep up.

● Information Breakdown

Even when buyers seek reliable information on long-term risk, it’s hard to find, with some government maps of severe flood zones dating to the 1970s. Homeowners in those areas must purchase flood insurance to get a federally insured mortgage, but people outside the zones—or those who own their home outright—have no such requirement. First Street Foundation says some 6 million homes that should be considered at severe risk of flooding lie outside those zones. And Milliman estimates there’s $520 billion of unpriced flood loss in the housing market—a number that will only increase.

Then there’s the question of how much insurance should cost. Carly Fabian of consumer-rights group Public Citizen says buyers deserve access to average home insurance prices by ZIP code over time, which would help them assess where insurers believe risks are spiking and whether they’re paying inflated rates. But insurance companies have blocked such efforts, saying the information is proprietary. “They’ve proven unreliable narrators on climate,” Fabian says.

● The Government Backstop

In the 1960s private insurers largely pulled the plug on residential flood coverage, deeming it too risky. The federal government stepped in with the National Flood Insurance Program (NFIP), which racks up about $1.4 billion a year in losses because it can’t charge market rates. Similar state programs in California, Florida and Louisiana only insure homes that can’t get private coverage, but with insurers backing out, they’re adding customers rapidly. Florida’s Citizens Property Insurance Corp. is already the largest single insurer in the state.

The Federal Emergency Management Agency is promising reforms that will bring NFIP premiums more in line with climate risks, but Keys is skeptical. “It’s like a dad threatening to turn the car around when the kids aren’t behaving properly,” he says. “The government isn’t not going to step in and bail out people when there’s a disaster.”

● Not Yet a Deal-breaker

Premiums are rising, but so is everything else—and insurance isn’t yet expensive enough to deter buyers, with utilities and property taxes representing a bigger share of the price of a house. Even at twice the cost, insurance would “still only account for a small proportion of asset prices,” says Danny Ismail, a researcher at analytics company Green Street. But investors in mortgage-backed securities may soon start demanding coverage for the full length of the loan. “The common denominator is that risk does not really belong to the insurance companies; it belongs to the community,” Watkins says. “The insurance market is not sufficient to tackle this problem.”